Two businesses with identical EBITDA can trade at 2× or 5×. The difference isn't in the P&L — it's in what the P&L is built on. Buyers aren't pricing past performance. They're pricing the probability that revenue survives after the founder walks out.

Most founders think the path to a higher valuation runs through revenue.

More clients. Better margins. A strong year.

Then the business broker delivers a number that looks right on paper. Brokers are paid on commission — their incentive is to get you to list, not to tell you what buyers will actually pay. So the pitch is optimistic. The asking price reflects the best-case scenario.

Buyers know this. And buyers do diligence.

What surfaces in due diligence — customer concentration, founder-dependent revenue, unpredictable financials — doesn't disappear because a broker chose not to mention it. It just shows up later, as a re-trade, a price reduction, or a deal that quietly collapses. A waste of time for everyone involved, including the founder who spent 12 months preparing for an exit that never closed.

That gap — between what brokers quote and what buyers will actually pay — almost never comes down to performance.

It comes down to structure.

Two service businesses. Same EBITDA. Same industry. Same revenue trajectory.

One sells at 2×. The other at 5×.

The difference isn't in the P&L. It's in what the P&L is built on.

Buyers aren't pricing your current business. They're pricing the probability that your cash flows survive after you leave. That calculation — risk — is what moves multiples up or down. Lower perceived risk equals higher multiple. It's not complicated. It's just not what most founders optimize for.

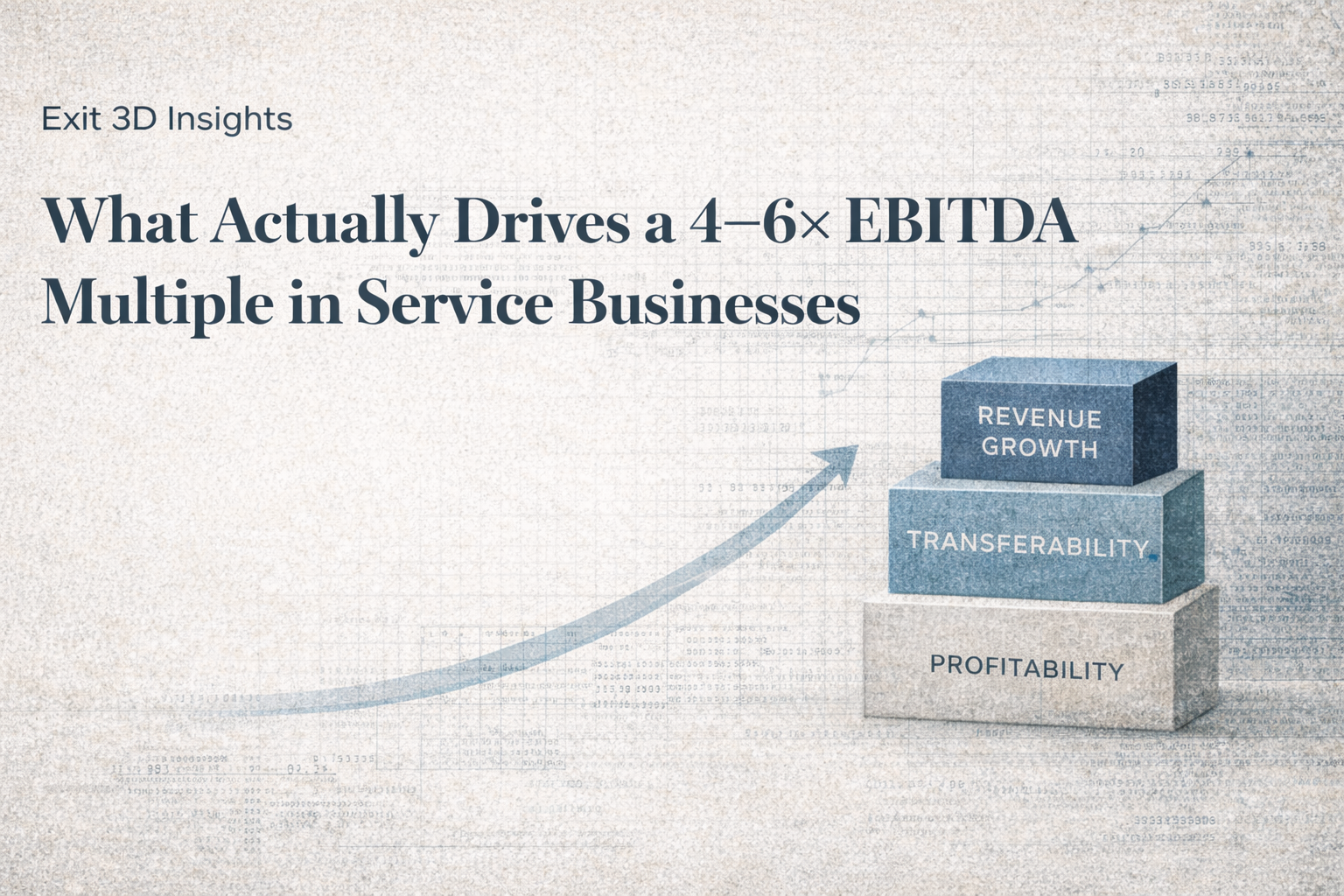

In the lower middle market, service businesses typically trade between 3× and 6× EBITDA. The premium end of that range isn't reserved for the fastest-growing companies. It's reserved for the ones that are hardest to break.

It's structural. Not cosmetic.

A 2× business:

A 5× business:

Buyers aren't evaluating what you built. They're evaluating what remains after you leave.

Recurring revenue isn't just a business model preference. It's a valuation driver.

Businesses with genuine recurring components — contracts, retainers, subscriptions, high renewal rates — routinely reach 4–6× EBITDA and above. Businesses where every dollar has to be re-earned each quarter often cap out at 2–3×.

Project-based revenue models are particularly penalized. Not because project work is bad business — but because it produces a pattern buyers can't model with confidence. One strong quarter followed by a slow pipeline isn't volatility. In a buyer's underwriting model, it's risk.

What buyers evaluate: contracts in place, renewal history, average contract length, revenue volatility year over year. The pattern matters more than the peak.

One volatile year surrounded by strong ones doesn't erase the discount. Buyers look at the full three-year trajectory plus trailing twelve months. A business that went $1M → $700K → $1.3M doesn't look like a recovery. It looks like a business with an unexplained dip that could happen again.

"Short-term spikes don't close deals. Predictable trailing performance does."

A single client representing more than 20–30% of revenue is a red flag. Above 40%, it's often a deal-killer — or a significant re-pricing event.

Concentration isn't just a risk for the buyer. It's leverage handed over at the negotiating table. The conversation shifts from "what is this business worth" to "what happens if that client leaves after close." Buyers protect themselves with lower multiples, earnouts, or holdbacks.

High logo churn compounds the problem. If the client base turns over frequently — even if total revenue holds — buyers see a business that has to keep re-acquiring its own revenue. That's expensive to run and fragile to own.

Diversification doesn't happen in the 6 months before you list. It takes 2–3 years to show up as a clean, defensible pattern in your financials. A business that fixes concentration one year before exit looks like a business that knew it had a problem. Not a business that solved it.

This is the most powerful lever — and the most overlooked.

Reducing owner dependency can add 1–1.5× to your multiple on its own.

The question every buyer asks, explicitly or not: what happens to revenue when this person walks out the door?

If the answer involves risk — key relationships that don't transfer, knowledge that lives in someone's head, a sales process that requires the founder's involvement to close, delivery that relies on the founder's personal credibility — that risk gets priced in. Sometimes as a lower multiple. Sometimes as a multi-year transition agreement that keeps the founder tied to the business long after they wanted to be done.

Founder-led businesses aren't unsellable. Founder-dependent businesses are expensive to buy. There's a difference.

The businesses that command premium multiples are the ones where the founder can take two weeks off without the pipeline stalling, delivery slipping, or clients calling to check in.

Referral-based growth is not a system. It's a pipeline that exists at the mercy of relationships, timing, and goodwill.

Buyers want to see how the business generates demand. Not just that it does — but how, through what channels, at what cost, with what consistency.

Referrals are fine as a channel. They're dangerous as the only channel. A business where 80% of new revenue comes from word of mouth has an acquisition engine that a buyer can't replicate, can't scale, and can't underwrite with confidence.

What commands a premium:

A business that knows how it grows is a business a buyer believes they can scale. That belief is worth multiples.

Processes that live in someone's head don't transfer. They evaporate at close.

This is one of the most common diligence failures in service businesses. The business works — deliveries happen, clients are happy, revenue comes in — but when a buyer asks how, the answer is a collection of tribal knowledge, informal relationships, and undocumented workflows.

That's not a business. That's a job with a team attached.

Documented systems — SOPs, CRM discipline, pipeline visibility, reporting infrastructure, delivery consistency — reduce execution risk in the buyer's model. That reduction translates directly into willingness to pay more.

Buyers also look at management depth. A business that requires the founder to be present for key decisions isn't structurally independent. One that has a capable team making operational decisions, with the founder focused on strategy, is a fundamentally different acquisition.

Strong operational infrastructure can add 0.5× or more to your multiple. The businesses that reach 6–8× EBITDA typically combine this with everything above.

Founders spend most of their energy trying to grow EBITDA. That's not wrong.

But the math on multiple expansion is more powerful — and most founders never run it clearly.

Same EBITDA. Two different outcomes:

Scenario A

EBITDA $1,000,000

Multiple X2

Valuation $2,000,000

Scenario B

EBITDA $1,000,000

Multiple X5

Valuation $5,000,000

That $3M difference didn't come from working harder. It came from building differently.

Now combine multiple expansion with EBITDA growth over a 2–3 year structured runway — which is exactly what exit-focused growth produces — and the gap widens further. A business at $800K EBITDA at 2× is worth less than a business at $700K EBITDA at 5×. The multiple matters more than most founders realize until it's too late to change it.

The default playbook before an exit: grow revenue, improve margins, hire more people.

None of that is wrong. All of it is insufficient.

Buyers don't pay for effort. They pay for predictability, transferability, and risk reduction. Revenue growth built on founder relationships, a single dominant client, or one acquisition channel doesn't produce a better multiple — it produces more revenue at the same, or worse, multiple. This is precisely why most service businesses end up at 1–3× EBITDA regardless of their revenue trajectory: the structural issues that cap multiples aren't addressed, because founders optimize for growth instead of durability.

The other common mistake: timing. Founders assume they can start cleaning up the business 6–12 months before they want to sell. By then, the financial track record that buyers evaluate is largely written. One strong year with visible structural improvements doesn't erase 2 years of volatility, concentration, or founder dependency. It just raises questions about why things changed right before the sale.

The structural work has to come before the growth, or alongside it. Not after.

The answer most founders get wrong: the year before they want to sell.

Buyers look at three full years of financial history plus trailing twelve months. That means the work that affects your valuation is largely complete before the process starts.

A business that fixes its concentration, reduces founder dependency, and builds a documented acquisition engine in the 12 months before listing is still a business with one good year. That's not a premium multiple. That's a slightly less discounted one.

The founders who sell at 5–6× started building for it 2–3 years out. Not because they planned to sell at a specific date — but because they were building something that could run without them. The exit readiness was a byproduct of how the business was structured, not a last-minute project.

Not the revenue number. That's the starting point of the conversation, not the conclusion.

They'd look at where the revenue comes from, how repeatable it is, what the three-year trajectory looks like, whether concentration creates a single point of failure, what happens to the pipeline when the founder is unavailable, and whether the systems that support the business would survive a change in ownership.

Most service businesses fail that evaluation — not because they're badly run, but because they were never built with this lens in mind.

That lens determines what you're worth. And it rewards the founders who thought about it early.

If a buyer opened your books today — not your best month, your full three-year history — what would increase their confidence?

And what would give them leverage to negotiate you down?

The earlier you answer that question honestly, the more control you retain over the outcome.

Most lower mid-market service businesses trade between 1× and 6× EBITDA. The majority land in the 2–3× range due to structural risk factors — concentrated clients, founder-dependent revenue, and unpredictable financials. Businesses with predictable recurring revenue, diversified clients, documented systems, and reduced founder dependency consistently reach 4–6× and above.

The five levers that move multiples are revenue predictability, customer diversification, founder independence, a structured acquisition engine, and documented operational systems. These aren't cosmetic improvements — they require 2–3 years of deliberate structural work to show up as a defensible track record. A single strong year doesn't change the multiple; a consistent three-year trajectory does.

When a single client represents 20–30% or more of revenue, buyers model the downside: what does this business look like if that client leaves after close? The answer justifies a lower multiple, earnout conditions, or holdback provisions. Concentration also hands negotiating leverage to the buyer — the conversation shifts from what the business is worth to what happens if one conversation goes wrong.

Reducing owner dependency can add 1–1.5× to the multiple on its own. When revenue generation, client retention, and key decisions run through the founder, buyers model post-acquisition performance as conditional on the founder staying — which they are trying to exit. A business that can operate, generate pipeline, and retain clients without the founder is structurally worth more, because the buyer's investment isn't contingent on one person.

%20(1)%201.webp)

.png)

.png)

.svg)

.svg)

.svg)